Let me be honest with you — I almost paid $4,200 out of pocket for a procedure my insurance was supposed to cover. Not because my plan was bad, but because I didn’t know how to use it properly.

That moment of panic in the billing office? It changed how I look at health insurance forever. I started digging into every clause, every loophole, every trick that patient advocates and seasoned policyholders actually use. And what I found genuinely surprised me.

Most people treat their insurance card like a get-out-of-jail-free card. Swipe it, hope for the best, and deal with the bill shock later. But the patients who actually save money — sometimes thousands — are doing something different. They’ve learned to work with the system instead of just hoping it works for them.

Here’s what I learned.

1. Always Request an Itemized Bill — Then Challenge Every Line

This one sounds obvious, but almost nobody actually does it.

When you get a medical bill, it usually shows one big number. What it doesn’t show you is how that number was calculated. The moment I asked for an itemized bill after my ER visit, I found three charges for supplies I never used — including a “surgical kit” for what was essentially a bandage change.

Insurance companies often pay inflated amounts for line items that don’t even apply to your care. And when they overpay, guess who makes up the difference through higher premiums over time? You do.

What to do:

- Call the billing department within 30 days of receiving any bill

- Ask specifically for an itemized statement (also called an “UB-04” for hospital stays)

- Compare each charge against your Explanation of Benefits (EOB) from your insurer

- Flag anything that doesn’t match your actual treatment

One thing that helped me was using a free tool like Goodbill or Medliminal — they review medical bills for errors and can negotiate on your behalf. Some work on a percentage of savings basis, so there’s no upfront cost.

A study published by NerdWallet found that roughly 80% of medical bills contain at least one error. That’s not a fringe case — that’s nearly every bill.

2. Understand the Difference Between “Covered” and “Pre-Authorized”

This was my $4,200 lesson.

My doctor recommended a specific imaging scan. I called my insurance, confirmed it was “covered under my plan,” and scheduled it. What I didn’t do was verify that this specific facility was in-network AND that the procedure was pre-authorized for my diagnosis code.

Two different things entirely.

A procedure being covered means it’s on your plan’s list of eligible services. Pre-authorization means your insurer has approved it for you, at that facility, for that reason, before it happens. Skip pre-auth and you could end up with a denial — even for something technically covered.

Here’s a quick checklist to run before any procedure:

| Step | What to Do |

|---|---|

| Confirm coverage | Call the member services number on your card |

| Verify in-network | Check the provider directory online (don’t just trust what the office says) |

| Request pre-authorization | Ask your doctor’s office to submit it — don’t assume they will |

| Get a reference number | Every call to your insurer should end with a confirmation number |

| Ask about billing codes | Make sure the CPT code your doctor uses matches what insurance approved |

The reference number part is critical. If a claim gets denied and you have no record of the approval conversation, you have almost nothing to stand on in an appeal.

3. Use Your Appeal Rights — Most People Never Do

A denial is not a final answer. I can’t stress this enough.

When my imaging claim was initially denied, the letter felt so official and final that I almost just paid it. But insurance companies are required by law to have an appeals process — and they count on most people not using it.

According to the Kaiser Family Foundation, fewer than 0.2% of denied claims are ever appealed. Yet when people do appeal, they win a significant portion of the time — especially for medical necessity denials.

Here’s roughly how an appeal works:

Step 1: Request the specific denial reason in writing. “Not medically necessary” or “out of network” — you need the exact language and the specific code.

Step 2: Get a letter of medical necessity from your doctor. This is a document explaining why this particular treatment was required for your condition. Most doctors will write one if you ask.

Step 3: Submit a formal internal appeal. Most insurers have a 30–60 day window from the denial date. Include the medical necessity letter, any relevant medical records, and a brief personal statement.

Step 4: If internal appeal fails, request an external review. An independent third-party reviews your case. Under the ACA, insurers must comply with external review decisions.

I’ve helped two family members win appeals this way. One got a $6,000 claim reversed. The other got a mental health treatment approved after three denials. It takes some paperwork and persistence, but it works.

If you’re traveling abroad for treatment, check out this guide on 9 Important Questions to Ask Before Getting Surgery Overseas — it covers what insurance questions to ask before you’re in a foreign billing office.

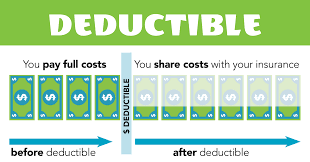

4. Time Your Medical Spending Around Your Deductible Year

Nobody talks about this, and it’s one of the most practical money moves you can make.

Your insurance deductible resets every plan year — usually January 1st or on your policy anniversary date. Once you’ve hit your deductible, insurance starts covering a much larger share of your costs. But most people don’t strategically plan around this.

Here’s what smart patients do:

If you’ve already met your deductible for the year: Schedule elective procedures, dental work (if linked to your plan), vision needs, specialist visits, and any planned imaging before your plan year resets. You’ve essentially already “bought” your coverage for that period.

If you haven’t met your deductible and it’s late in the year: Run the math. Would it make sense to push a non-urgent procedure to January, when your slate is clean? Sometimes yes, sometimes no — depends on your specific numbers.

A rough decision table:

| Situation | Best Move |

|---|---|

| Deductible met, year ending soon | Stack elective procedures NOW |

| Deductible not met, procedure optional | Evaluate cost vs. next year reset |

| Chronic condition, high annual usage | Choose lower deductible plan at open enrollment |

| Generally healthy, rare visits | High-deductible plan + HSA often saves more |

Speaking of HSAs — if you’re on a high-deductible plan and not using a Health Savings Account, you’re leaving tax-advantaged money on the table. HSA contributions reduce your taxable income, the money grows tax-free, and withdrawals for medical expenses are tax-free. It’s one of the only triple-tax-advantaged accounts that exists.

5. Know Your Out-of-Network Rights (They’re Bigger Than You Think)

Going out-of-network doesn’t always mean you’re on your own.

In the US, the No Surprises Act (effective 2022) prevents balance billing in emergency situations and for some specialist care — even if that specialist is out-of-network. This was a huge change. Before it, you could have emergency surgery at an in-network hospital and still get a massive bill from the out-of-network anesthesiologist.

Now, in most cases, you can only be billed your in-network cost-sharing amount for emergency services, regardless of network status.

What you can do right now:

- Check if your state has its own surprise billing protections (many states have even stronger laws)

- If you received a surprise bill after January 2022 for emergency care, you may be able to dispute it through the federal No Surprises Help Desk

- For non-emergency out-of-network care, always get a Good Faith Estimate before receiving treatment

The Good Faith Estimate requirement — also part of the No Surprises Act — means any provider must give you a written estimate of expected charges if you’re uninsured or self-pay. Some providers will do it for insured patients too if you ask.

For those navigating global coverage, this piece on 7 Smart Insurance Hacks for Global Coverage is worth bookmarking — especially if you travel often or have family abroad.

6. Maximize Benefits You’re Probably Ignoring

I did a full review of my insurance plan last year and was genuinely embarrassed by what I found.

My plan covered:

- Annual gym membership reimbursement (up to $300)

- Telehealth visits at $0 copay

- Mental health apps like Calm or Headspace (partially reimbursed)

- A nurse hotline for free medical advice

- Discounts on vision and dental through affiliated networks

- Free second opinion services for serious diagnoses

I had been paying out of pocket for some of these for years.

Most insurance plans — especially employer-sponsored ones — include a range of wellness benefits that never get advertised loudly. They’re buried in the member portal or benefits summary.

Here’s how to actually find them:

- Log into your insurer’s member portal (not just the card) and look for a “Benefits & Coverage” or “Wellness Programs” section

- Search for your plan’s Summary of Benefits and Coverage (SBC) document — all plans are required to provide this

- Call member services and literally ask: “What benefits am I currently not using?” — some reps will actually walk through it with you

- Check if your employer has a benefits coordinator or HR rep who specializes in this

Benefits commonly overlooked by plan type:

| Plan Type | Often-Missed Benefits |

|---|---|

| Employer-sponsored PPO | Wellness reimbursements, EAP programs |

| Medicare Advantage | Dental, vision, hearing, OTC allowances |

| Marketplace ACA plans | Preventive care at $0, mental health parity |

| High-deductible + HSA | Investment options within HSA accounts |

One thing I started doing is setting a calendar reminder every October — right before open enrollment — to do a full benefits audit. It takes maybe 90 minutes, and last year it saved me over $400 in benefits I would have otherwise missed.

If you want to go deeper on this, especially around maximizing what you’re already paying for, this guide on 10 Powerful Ways to Maximize Insurance Benefits is genuinely one of the most practical reads I’ve come across.

Common Mistakes That Cost People the Most

Before I wrap up, here’s a quick hit list of things I see people mess up repeatedly — including myself at one point:

- Assuming in-network = covered: In-network means discounted rates, not automatic full coverage

- Ignoring EOBs: That “Explanation of Benefits” document isn’t junk mail — it’s your record of what was processed and why

- Not calling before non-emergency procedures: A 10-minute call can prevent a $3,000 surprise

- Letting FSA money expire: Flexible Spending Account funds are use-it-or-lose-it — check your balance in November

- Choosing the cheapest premium without checking the network: A $50/month savings means nothing if your doctor isn’t covered

One Last Thing

The insurance system is complicated by design — not by accident. But that doesn’t mean you’re powerless inside it.

Every hack I’ve shared here is something a regular person can actually use. No law degree required. No special connections. Just knowing where to look, what questions to ask, and when to push back instead of just paying.

The patients who save the most money aren’t necessarily the healthiest or wealthiest. They’re the most informed.

And if you’re looking to build on this knowledge — especially when it comes to reducing your actual premium costs without giving up the coverage that matters — this article on 11 Proven Ways to Slash Premiums Without Losing Your Coverage is the next logical step.

Start with one hack. Audit your benefits. Request one itemized bill. Make one call. That’s usually how the savings start.