There’s a quiet moment that often comes before financial trouble sets in. It doesn’t look dramatic. No alarms go off. It might just be a missed payment, a borrowed amount to cover something urgent, or a small purchase made with the thought of “I’ll deal with it later.” That moment, repeated enough times, builds the foundation of a debt trap.

Debt traps rarely begin with reckless decisions. More often, they grow from urgency, lack of planning, or simply not knowing better options. The good news is that avoiding them doesn’t require extreme financial discipline or high income. It requires awareness, quick decision-making, and a few practical strategies that can be applied immediately.

The following ten fast financing hacks are designed to help you stay ahead of debt, not react to it after it’s already taken hold.

Understanding how debt traps form

Before jumping into solutions, it helps to understand the pattern behind most debt cycles:

| Stage | What Happens | Risk Level |

|---|---|---|

| Initial Shortfall | Expenses exceed income briefly | Low |

| Quick Borrowing | Credit cards, loans, or borrowing fills gap | Medium |

| Accumulated Interest | Interest begins compounding | High |

| Payment Strain | Monthly obligations increase | Very High |

| Debt Spiral | New debt taken to repay old debt | Critical |

The goal is simple: interrupt this cycle early.

Hack 1: Create a 48-hour decision rule for borrowing

Urgency often leads to poor financial decisions. A simple rule—waiting 48 hours before taking any non-emergency loan—can prevent impulsive borrowing.

During this waiting period, ask yourself:

- Is this expense unavoidable?

- Can it be delayed or reduced?

- Is there a non-debt alternative?

Even this short pause introduces clarity. Many expenses lose their urgency when given time.

Hack 2: Split expenses into “essential now” vs “can wait”

Not all expenses deserve immediate financing. Categorizing costs helps you avoid unnecessary borrowing.

| Expense Type | Examples | Action Strategy |

|---|---|---|

| Essential Now | Rent, medicine | Prioritize immediately |

| Important Soon | Repairs, school fees | Plan within budget |

| Can Wait | Gadgets, upgrades | Delay or skip |

This simple classification reduces emotional spending and protects you from avoidable debt.

Hack 3: Negotiate bills before financing them

Many people jump to loans before attempting negotiation. But service providers—hospitals, utilities, even schools—often offer payment plans or temporary relief.

| Expense Category | Possible Negotiation Option |

|---|---|

| Medical bills | Installment plans, discounts |

| Utility bills | Extended due dates |

| Rent | Partial payments, delayed balance |

Negotiation doesn’t eliminate the cost, but it spreads it out—often without interest.

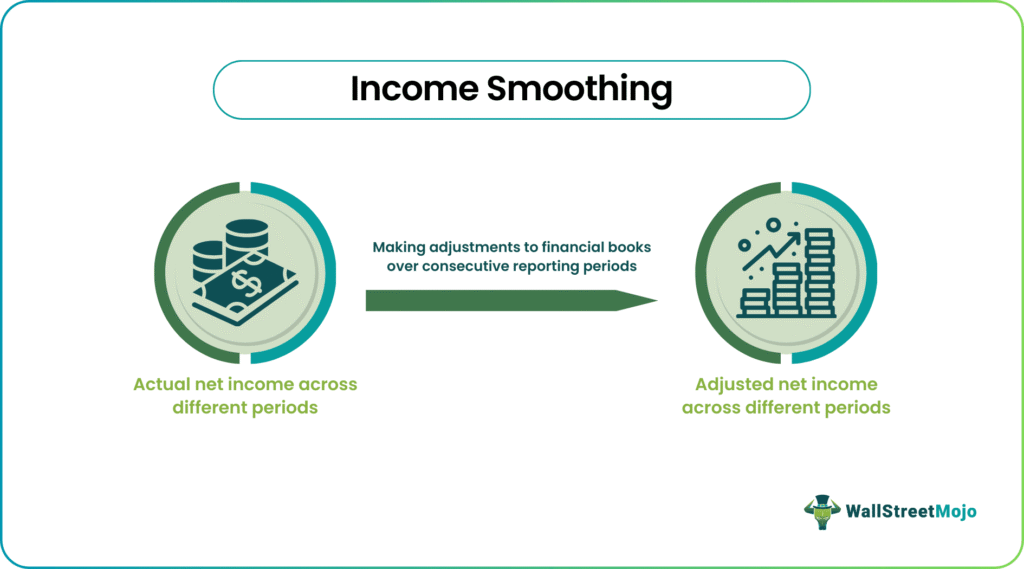

Hack 4: Use income smoothing instead of borrowing

Income gaps are a major trigger for debt. Instead of borrowing during low-income periods, aim to smooth your cash flow.

This can be done by:

- Saving small amounts during high-income periods

- Keeping a buffer equal to at least one month’s expenses

- Timing major payments with income cycles

Here’s a simple illustration:

| Scenario | Result |

|---|---|

| No buffer, income dip | Borrowing required |

| With buffer | No borrowing needed |

The difference lies in preparation, not income size.

Hack 5: Cap your monthly debt exposure

One of the fastest ways into a debt trap is overcommitting future income. Setting a strict cap on how much of your income can go toward debt repayments keeps things manageable.

A basic guideline:

| Income Portion Used for Debt | Financial Impact |

|---|---|

| Low percentage | Sustainable |

| Moderate percentage | Manageable but tight |

| High percentage | High risk of default |

Even if lenders approve larger amounts, that doesn’t mean you should accept them.

Hack 6: Replace high-interest debt with smarter alternatives

Not all debt is equally harmful. High-interest borrowing—like credit cards or payday loans—can escalate quickly.

Replacing them with lower-cost options can reduce pressure:

| Debt Type | Typical Cost Level | Better Alternative |

|---|---|---|

| Credit card balance | Very high | Personal loan (lower rate) |

| Payday loan | Extremely high | Family loan or installment |

| Informal borrowing | Variable | Structured repayment plan |

The goal is not to accumulate more debt, but to reduce the cost of existing obligations.

Hack 7: Track every borrowed amount in one place

Disorganized borrowing is dangerous. When loans are scattered across different sources, it becomes difficult to track obligations.

A simple tracking table helps:

| Source | Amount | Interest | Due Date | Status |

|---|---|---|---|---|

| Bank loan | Medium | Moderate | Monthly | Ongoing |

| Friend | Small | None | Flexible | Pending |

| Credit card | High | High | Monthly | Critical |

Seeing everything in one place creates awareness and prevents missed payments.

Hack 8: Build a “no-loan emergency toolkit”

Before reaching for a loan, consider alternatives that don’t involve debt:

| Situation | Alternative Solution |

|---|---|

| Medical need | Community clinics |

| Urgent cash | Sell unused items |

| Shortfall | Freelance or gig work |

These options may require effort, but they avoid long-term financial strain.

Hack 9: Use micro-saving strategies to prevent borrowing

Debt often fills small gaps that could have been covered with better saving habits.

Micro-saving strategies include:

- Rounding off expenses and saving the difference

- Setting aside small daily amounts

- Saving unexpected income (bonuses, gifts)

| Daily Saving Amount | Monthly Total |

|---|---|

| Very small | Meaningful |

| Slightly higher | Significant |

These small reserves act as a first line of defense against borrowing.

Hack 10: Learn to recognize early warning signs

Debt traps don’t appear suddenly—they build gradually. Recognizing early signals can help you act before things escalate.

Common warning signs include:

- Using new loans to pay old ones

- Missing payment deadlines

- Relying on credit for basic expenses

- Feeling uncertain about total debt

| Warning Sign | Suggested Action |

|---|---|

| Missed payments | Reassess budget immediately |

| Rising interest costs | Refinance or reduce debt |

| Frequent borrowing | Pause and review spending |

Awareness is often the difference between control and crisis.

The psychology behind avoiding debt

Financial decisions are rarely just about numbers. Emotions—fear, urgency, social pressure—play a significant role. Quick financing hacks work best when combined with a shift in mindset.

Instead of asking “How can I pay for this right now?” try asking:

“What happens if I don’t borrow for this?”

This small shift often reveals alternatives that weren’t obvious before.

Long-term impact of short-term decisions

It’s easy to underestimate how small borrowing decisions add up over time.

| Decision Type | Short-Term Effect | Long-Term Outcome |

|---|---|---|

| Frequent borrowing | Immediate relief | Financial stress |

| Controlled spending | Slight discomfort | Stability and freedom |

The difference is not dramatic in the moment, but it becomes significant over months and years.

Combining hacks for stronger results

Each of these hacks works individually, but their real strength lies in combination.

For example:

- Using the 48-hour rule + expense categorization reduces unnecessary borrowing

- Tracking debt + capping exposure prevents overload

- Micro-saving + emergency toolkit reduces dependence on loans

When applied together, they form a system that protects you from falling into debt traps.

A practical monthly framework

To make these hacks actionable, here’s a simple monthly structure:

| Week | Focus Area |

|---|---|

| Week 1 | Review expenses and categorize |

| Week 2 | Track and update debt status |

| Week 3 | Build savings buffer |

| Week 4 | Evaluate financial decisions |

This routine takes minimal time but creates consistent awareness.

FAQs

- What is the fastest way to avoid falling into debt

The fastest way is to pause borrowing decisions using a short waiting rule and evaluate whether the expense is truly necessary. - How much debt is considered safe

There is no universal number, but keeping debt repayments within a manageable portion of your income helps maintain stability. - Can small savings really prevent borrowing

Yes, even small savings can cover minor expenses that would otherwise require borrowing, reducing dependence on credit. - Is refinancing always a good idea

Refinancing can help if it reduces interest or simplifies payments, but it should not lead to taking on more debt. - What should I do if I’m already in a debt trap

Start by listing all debts, prioritizing high-interest ones, and exploring ways to reduce costs or increase income. - Are informal loans from friends safer than bank loans

They may have lower or no interest, but they still require responsibility and clear repayment terms to avoid personal strain.

Avoiding debt traps is less about perfection and more about awareness and timely action. These fast financing hacks are not complex systems—they are practical decisions that, when applied consistently, create a financial buffer strong enough to keep debt from taking control.