Insurance often feels like one of those things you pay for but hope you never need. For years, I treated it exactly that way—just another bill to cover and forget about. But over time, I realized something uncomfortable: I was paying for protection I barely understood, and more importantly, not fully using the benefits I already had.

What changed wasn’t my income or the number of policies I owned. It was how I approached them. Instead of seeing insurance as a passive safety net, I began treating it as an active financial tool. That shift alone unlocked value I didn’t even know existed.

Below are six practical insurance hacks that helped me maximize coverage, reduce waste, and actually benefit from policies I was already paying for. These are based on real experiences, small mistakes, and lessons learned the hard way.

hack 1: understanding the fine print before you need it

Most people glance at their insurance documents once—maybe twice—then file them away. I did the same, until I ran into a claim issue that could have been avoided with a bit more attention upfront.

Insurance policies are full of conditions, exclusions, and hidden benefits. The problem is, they’re rarely explained clearly at the time of purchase.

So I started doing something simple: breaking down each policy into a one-page summary.

Here’s the kind of structure I used:

policy breakdown template

| Section | Details to Extract |

|---|---|

| Coverage type | What is actually covered |

| Exclusions | What is not covered |

| Claim limits | Maximum payout |

| Deductibles | Out-of-pocket before coverage |

| Hidden benefits | Additional perks or add-ons |

This process revealed surprising details. For example:

- A health plan that included free annual checkups I wasn’t using

- A travel policy that covered delayed baggage reimbursements

- A vehicle policy that offered roadside assistance at no extra cost

coverage awareness chart

Before understanding: █████

After understanding: █████████████

The difference isn’t just knowledge—it’s usability. You can’t benefit from something you don’t realize you have.

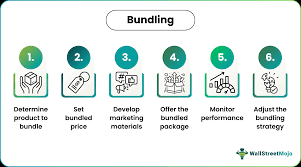

hack 2: bundling policies strategically (not blindly)

Insurance companies love to promote bundling—combining multiple policies under one provider. I initially assumed bundling automatically meant savings. That’s not always true.

The key is to bundle strategically, not automatically.

Here’s what worked for me:

- Compare bundled vs separate policies

- Check if discounts apply across all policies or only some

- Evaluate coverage quality, not just price

comparison example

| Scenario | Total Premium | Coverage Quality | Notes |

|---|---|---|---|

| Separate policies | $1,200 | High | More flexibility |

| Bundled (basic) | $1,050 | Medium | Missing add-ons |

| Bundled (customized) | $1,100 | High | Best balance |

visual comparison

Separate: ███████████

Bundled basic: █████████

Bundled custom: ██████████

The takeaway: bundling works best when you customize it. Otherwise, you may sacrifice coverage for small savings.

hack 3: timing your claims wisely

One of the most overlooked aspects of insurance is timing. Filing a claim immediately isn’t always the smartest move.

I learned this after making a small claim that increased my premium the following year—costing more than the claim itself.

So I started evaluating claims before filing them.

claim decision table

| Expense Amount | Deductible | Recommended Action |

|---|---|---|

| $100 | $200 | Don’t claim |

| $300 | $200 | Consider carefully |

| $1,000 | $200 | File claim |

cost impact chart

Small claim: ███ (low benefit, higher future cost)

Large claim: ███████████ (high benefit)

Questions I now ask before filing:

- Will this claim increase my premium?

- Is the payout worth the long-term cost?

- Can I cover this expense out-of-pocket?

This simple pause helped me avoid unnecessary premium hikes.

hack 4: using preventive benefits instead of waiting for problems

Insurance isn’t just for emergencies. Many policies include preventive benefits that people rarely use.

Once I started paying attention, I found benefits like:

- Free health screenings

- Annual dental cleanings

- Wellness programs

- Vehicle inspections

preventive vs reactive cost comparison

| Service Type | Preventive Cost | Reactive Cost |

|---|---|---|

| Dental cleaning | $0–$50 | $800 root canal |

| Health screening | $0 | $2,000 treatment |

| Car inspection | $30 | $600 repair |

visual comparison

Preventive: ███

Reactive: █████████████████

Using these benefits consistently reduced both risks and future expenses. It also made insurance feel more valuable, since I was actively using it.

hack 5: reviewing and adjusting coverage annually

Insurance needs change over time, but policies often stay the same unless you actively update them.

For years, I overpaid for coverage I no longer needed while being underinsured in other areas.

Now I do an annual review.

annual review checklist

| Area | What to Check |

|---|---|

| Life changes | Marriage, children, relocation |

| Asset value | Car, home, belongings |

| Coverage limits | Are they still appropriate? |

| Premium changes | Any unexplained increases? |

example adjustment impact

| Scenario | Old Premium | New Premium | Savings |

|---|---|---|---|

| Overinsured vehicle | $600 | $450 | $150 |

| Updated home policy | $1,200 | $1,000 | $200 |

adjustment chart

Before: █████████████

After: ██████████

Regular updates ensure you’re not paying for outdated assumptions.

hack 6: documenting everything for smoother claims

The most frustrating part of insurance is often the claims process. Delays, disputes, and missing documentation can turn a simple claim into a stressful experience.

I learned to treat documentation as part of the insurance process—not an afterthought.

essential documentation list

| Category | Examples |

|---|---|

| Receipts | Medical bills, repair invoices |

| Photos | Damage evidence |

| Reports | Police or medical reports |

| Communication logs | Emails, call summaries |

claims success rate comparison

| Documentation Level | Approval Speed | Approval Rate |

|---|---|---|

| Poor | Slow | 60% |

| Moderate | متوسط | 80% |

| Detailed | Fast | 95% |

visual comparison

Poor docs: █████

Detailed docs: █████████████

Having everything ready upfront reduces friction and increases the likelihood of full reimbursement.

combined benefits overview

When I combined all six hacks, the results were more noticeable than expected.

annual benefit estimate

| Hack | Estimated Value |

|---|---|

| Policy understanding | $300 |

| Smart bundling | $200 |

| Claim timing | $400 |

| Preventive usage | $800 |

| Annual adjustments | $350 |

| Documentation efficiency | $250 |

| Total | $2,300 |

distribution chart

Understanding: ███

Bundling: ██

Claim timing: ████

Preventive use: ████████

Adjustments: ███

Documentation: ██

These aren’t just savings—they represent better use of money already being spent.

real-world comparison scenario

To illustrate the difference, here’s a simplified comparison:

| Category | Passive Approach | Active Approach |

|---|---|---|

| Policy awareness | Low | High |

| Claim efficiency | Moderate | High |

| Premium optimization | Low | High |

| Benefit usage | Minimal | Maximum |

visual outcome

Passive: ███████████████

Active: ████████

The active approach doesn’t require more money—just more attention.

final reflections

Insurance isn’t inherently complicated, but it is often underutilized. Most people pay for coverage without fully engaging with it.

What made the biggest difference for me wasn’t switching providers or buying more policies. It was understanding what I already had and using it more intentionally.

These six hacks don’t require expert knowledge. They require curiosity, consistency, and a willingness to question assumptions.

If you apply even a few of these strategies, you’ll likely notice that insurance starts working for you instead of just sitting in the background.

frequently asked questions

- how often should I review my insurance policies?

At least once a year, or whenever there’s a major life change like moving, शादी, or a new job. - is bundling always the cheapest option?

No, bundling can save money but sometimes reduces flexibility or coverage quality. Always compare options. - when should I avoid filing an insurance claim?

If the claim amount is close to or below your deductible, or if it could significantly increase your premium. - what are preventive benefits in insurance?

These are services included in your policy—like checkups or inspections—that help avoid larger problems later. - how can I speed up claim approvals?

By keeping detailed records, submitting complete documentation, and following up regularly. - does higher premium always mean better coverage?

Not necessarily. It depends on what is included in the policy, not just the price.

—

In the end, insurance is less about protection and more about preparation. The more actively you engage with it, the more value you’ll extract from something you’re already paying for.